No saving power in loan default capital

Stapleton, John. The Australian [Canberra, A.C.T] 26 Sep 2008: 4.

Show highlighting

Abstract

"We have been paying the mortgage first and foremost and playing catch up with all the bills, gas, and electricity," Mr Holden said. "At the end of the week we have $10 left. But if we had fallen behind with the payments, we could have got the super, but you don't want to do that."

His wife, Julie Holden, 34, who handles the family finances, said: "The interest rate rises have really put pressure on our income. We pretty much can't go anywhere. What can you do about it? Grin and bear it."

"It is just very expensive," he said. "After paying the mortgage you still have to pay the bills and expenses with the kids. What you earn just goes. You have nothing to save for the future of the kids."

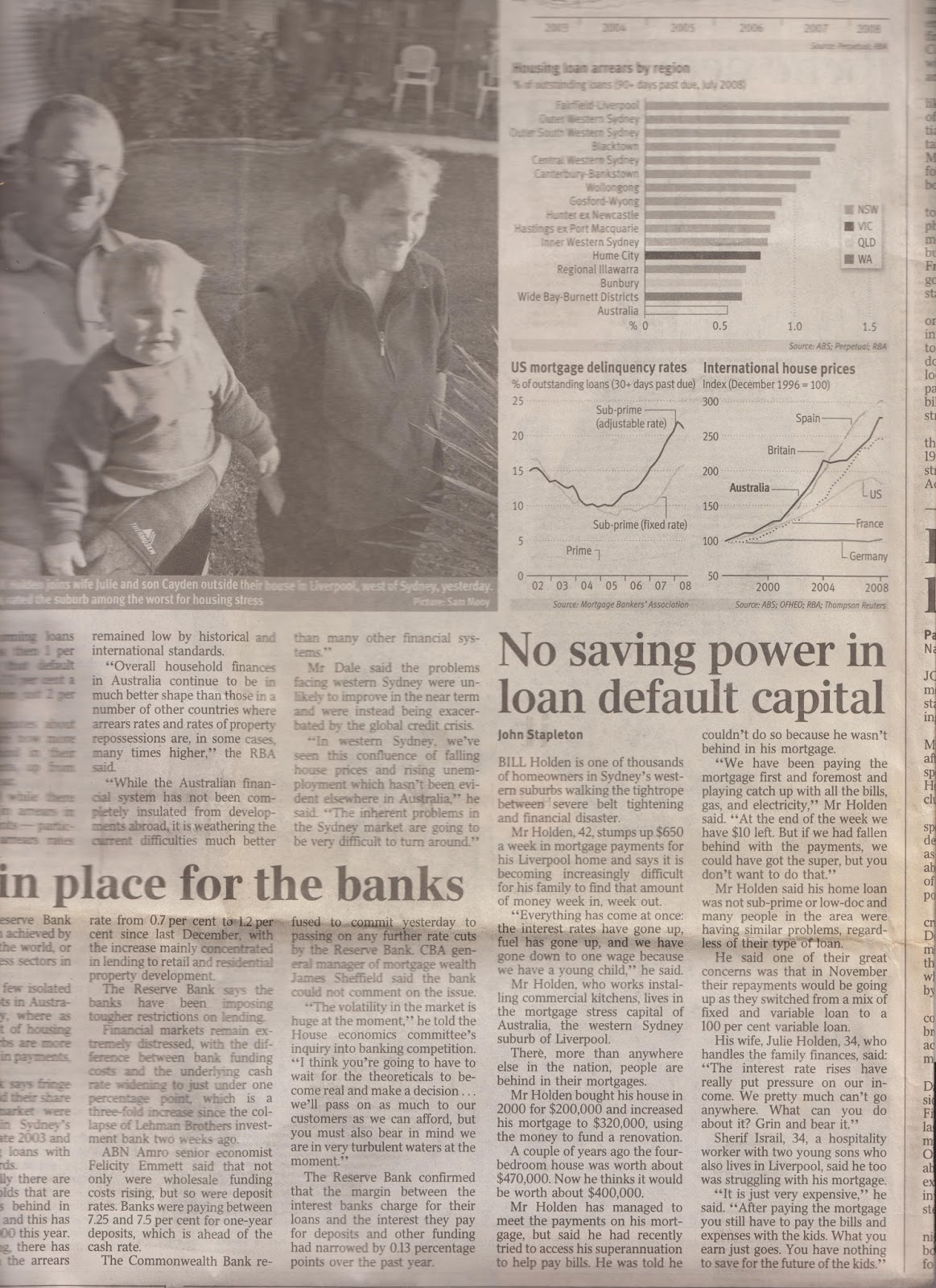

BILL Holden is one of thousands of homeowners in Sydney's western suburbs walking the tightrope between severe belt tightening and financial disaster.

Mr Holden, 42, stumps up $650 a week in mortgage payments for his Liverpool home and says it is becoming increasingly difficult for his family to find that amount of money week in, week out.

"Everything has come at once: the interest rates have gone up, fuel has gone up, and we have gone down to one wage because we have a young child," he said.

Mr Holden, who works installing commercial kitchens, lives in the mortgage stress capital of Australia, the western Sydney suburb of Liverpool.

There, more than anywhere else in the nation, people are behind in their mortgages.

Mr Holden bought his house in 2000 for $200,000 and increased his mortgage to $320,000, using the money to fund a renovation.

A couple of years ago the four-bedroom house was worth about $470,000. Now he thinks it would be worth about $400,000.

Mr Holden has managed to meet the payments on his mortgage, but said he had recently tried to access his superannuation to help pay bills. He was told he couldn't do so because he wasn't behind in his mortgage.

"We have been paying the mortgage first and foremost and playing catch up with all the bills, gas, and electricity," Mr Holden said. "At the end of the week we have $10 left. But if we had fallen behind with the payments, we could have got the super, but you don't want to do that."

Mr Holden said his home loan was not sub-prime or low-doc and many people in the area were having similar problems, regardless of their type of loan.

He said one of their great concerns was that in November their repayments would be going up as they switched from a mix of fixed and variable loan to a 100per cent variable loan.

His wife, Julie Holden, 34, who handles the family finances, said: "The interest rate rises have really put pressure on our income. We pretty much can't go anywhere. What can you do about it? Grin and bear it."

Sherif Israil, 34, a hospitality worker with two young sons who also lives in Liverpool, said he too was struggling with his mortgage.

"It is just very expensive," he said. "After paying the mortgage you still have to pay the bills and expenses with the kids. What you earn just goes. You have nothing to save for the future of the kids."

Credit: John Stapleton

No comments:

Post a Comment